Crypto Money Laundering Is Not Just a Big Bank Problem Anymore

A real crypto laundering case shows how fast money moves after a breach - and why small businesses need stronger systems, controls, and visibility before it happens to them.

Most small business owners hear the words crypto money laundering and immediately think:

“That has nothing to do with me.”

That is exactly the dangerous part.

The Kelp DAO incident is not only a crypto story. It is a warning about what happens when stolen digital money moves faster than companies, banks, payment processors, and compliance teams can react.

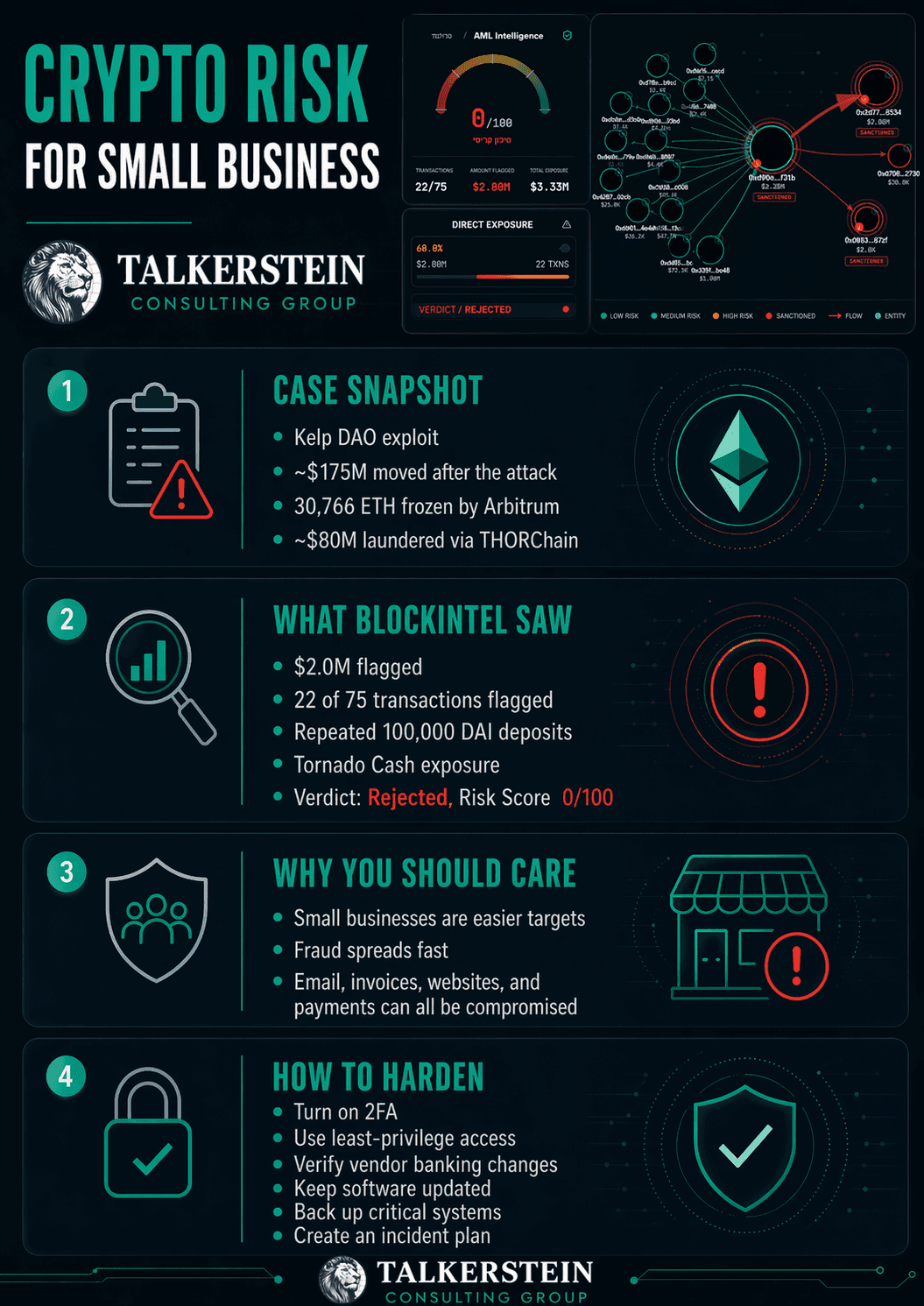

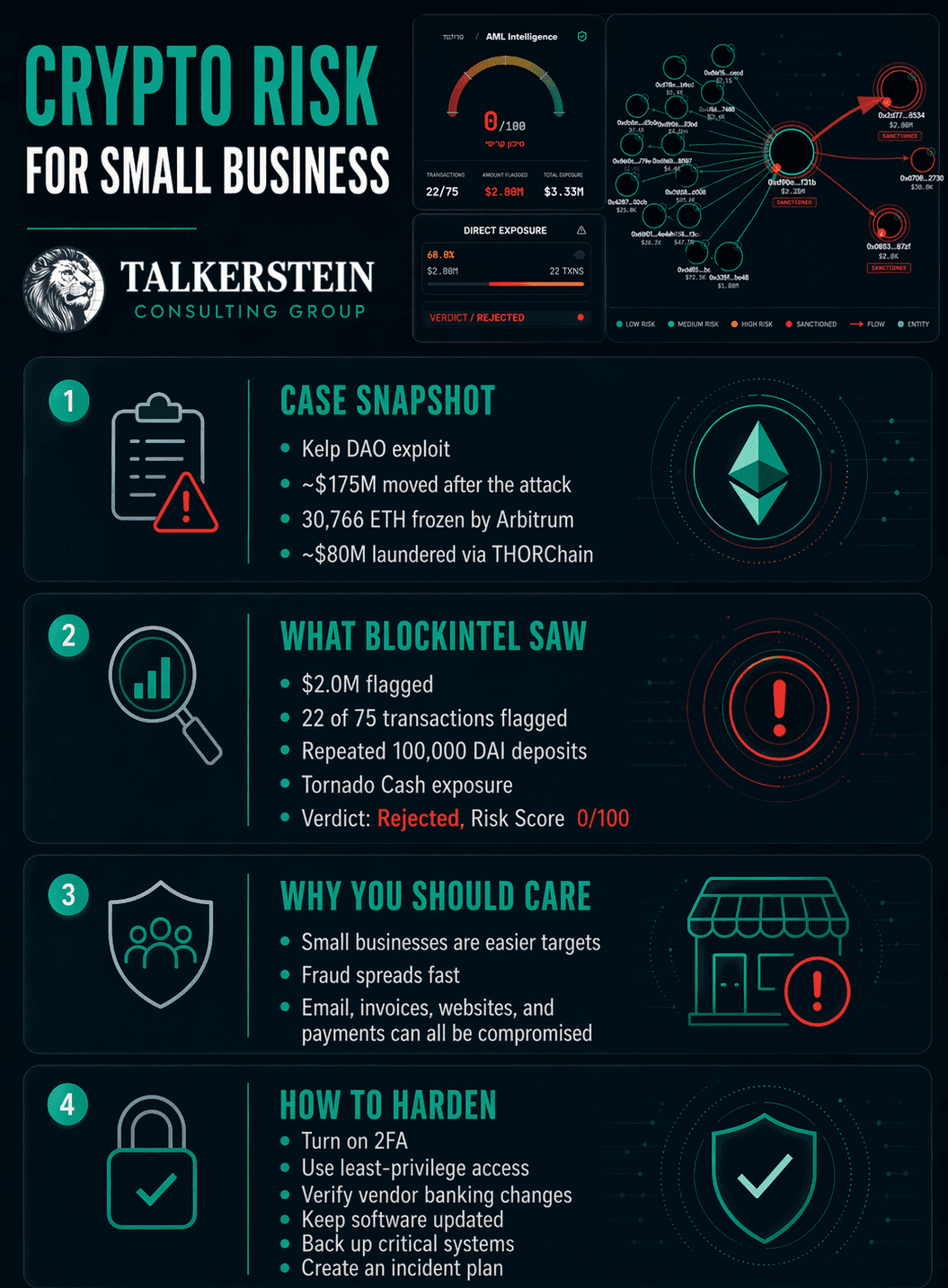

In this case, the attacker allegedly moved millions in Ethereum after the exploit, with funds reportedly routed through cross-chain protocols and mixers to make the money harder to trace. A BlockIntel AML report connected one reviewed wallet to critical-risk activity, including direct mixer exposure through Tornado Cash. The report gave the wallet a REJECTED verdict, a 0/100 risk score, and identified $2.00M in flagged volume across 22 flagged transactions out of 75 total transactions.

That sounds like something for a crypto exchange.

But the lesson is much bigger.

If your business accepts online payments, stores customer data, uses SaaS tools, runs eCommerce, works with contractors, receives wire transfers, uses digital wallets, or has any kind of online checkout, the same principle applies:

Money moves fast. Fraud moves faster. Weak systems get exposed first.

Why Small Businesses Should Care

Small businesses usually do not get attacked because they are famous.

They get attacked because they are easier.

A hacker does not need your company to be a bank. They just need one weak spot:

A reused admin password

A fake invoice email

A compromised WordPress plugin

An employee who clicks the wrong link

A payment page without proper controls

A Google Workspace account with no 2FA

A contractor with access who should have been removed months ago

A Shopify, WooCommerce, CRM, or email account with too many permissions

The Kelp DAO case shows what happens after money is already stolen. The funds do not just sit there. They move through layers, wallets, protocols, and mixers.

For a small business, the same pattern can happen in a simpler form.

A fraudster compromises an email account.

They change banking details on an invoice.

A customer pays the wrong account.

The money is moved again.

By the time anyone notices, recovery becomes difficult.

Different technology. Same problem.

Weak controls create expensive consequences.

This Is Not About Crypto. It Is About Business Infrastructure.

At Talkerstein Consulting Group, we do not look at this only as a blockchain issue.

We look at it as an infrastructure issue.

Most small businesses are building their digital operation in pieces:

Email from another

Payment processor separate from everything

Ads running independently

Staff using shared passwords

Contractors coming and going

No real documentation

No access control map

No incident response plan

That kind of setup may work when things are quiet.

It breaks when something goes wrong.

The real risk is not only that a business gets hacked. The real risk is that the business has no clean way to answer basic questions after the problem happens:

Who had access?

What changed?

Which account was compromised?

Which payment was legitimate?

Which transaction was suspicious?

Which customer was affected?

What should we shut down first?

Who needs to be notified?

What proof do we have?

The crypto world calls this AML and transaction monitoring.

For small businesses, we call it operational hardening.

Same idea: know what is happening, reduce blind spots, and respond before the damage spreads.

What the Kelp DAO Case Teaches Small Businesses

The BlockIntel report is useful because it shows the risk pattern clearly. The reviewed wallet was not rejected because of one vague concern. It was rejected because the system identified direct exposure to high-risk mixer activity and structured outgoing transactions linked to Tornado Cash.

That matters because modern fraud is usually not random.

It has patterns.

A small business can apply the same thinking:

A sudden login from a new country is a pattern

A new bank account added to a vendor profile is a pattern

A staff member requesting access to tools they do not normally use is a pattern

A customer asking to pay through an unusual method is a pattern

A refund request to a different card or wallet is a pattern

A sudden spike in failed checkouts or fake accounts is a pattern

You do not need to become a crypto analyst.

You do need systems that can spot unusual behaviour before it becomes a loss.

The Small Business Reality

Most small businesses are not underprotected because they do not care.

They are underprotected because everything feels urgent.

Sales comes first.

Customers come first.

Cash flow comes first.

The website has to launch.

The ads have to run.

The team needs access.

The client needs the invoice.

Security and compliance get pushed to “later.”

But “later” is usually when the damage has already happened.

A hardened business is not a paranoid business. It is a business that has basic discipline.

Good security does not have to be complicated. It has to be consistent.

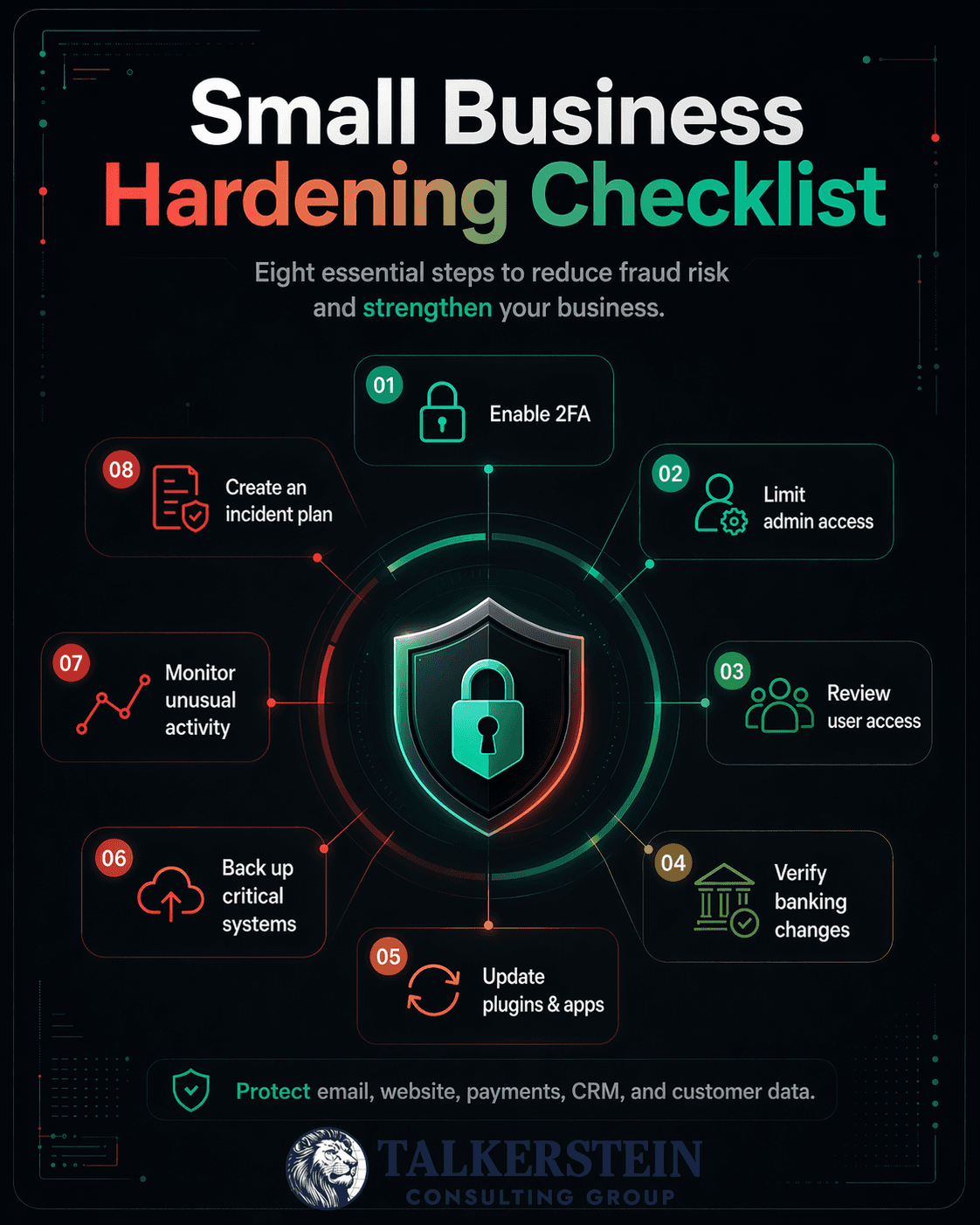

What TCG Recommends for Small Businesses

Every small business should have a basic digital risk foundation.

Not enterprise-level bureaucracy.

Just practical controls.

Start with the systems that control money, identity, and customer trust:

Email accounts

Website admin accounts

Payment processor accounts

Bank and accounting access

CRM access

Domain and hosting access

Social media accounts

Ad accounts

Customer database access

Contractor and employee permissions

These are the keys to the business.

If they are messy, the business is exposed.

The Main Takeaway

The Kelp DAO story is dramatic because the numbers are huge and the funds moved through crypto infrastructure.

But the underlying lesson applies to every business:

Once money or access is compromised, speed matters.

You need visibility before the incident.

You need controls during the incident.

You need documentation after the incident.

Small businesses cannot afford to operate like their systems are casual.

Your website, email, CRM, payments, ads, and data are not “tech stuff.”

They are business infrastructure.

And infrastructure needs to be hardened.

How can TCG help?

TCG helps small businesses clean up and harden their digital infrastructure across websites, email, hosting, CRM, payments, automations, analytics, and access control. The goal is simple: make the business easier to manage, harder to compromise, and better prepared when something goes wrong.

Quick Links

" height="149.2535067768008px" id="IOCTf08f5" width="1199.9520008715217px"/></svg>)